How does Aotearoa compare to Australia?

Modal to play video

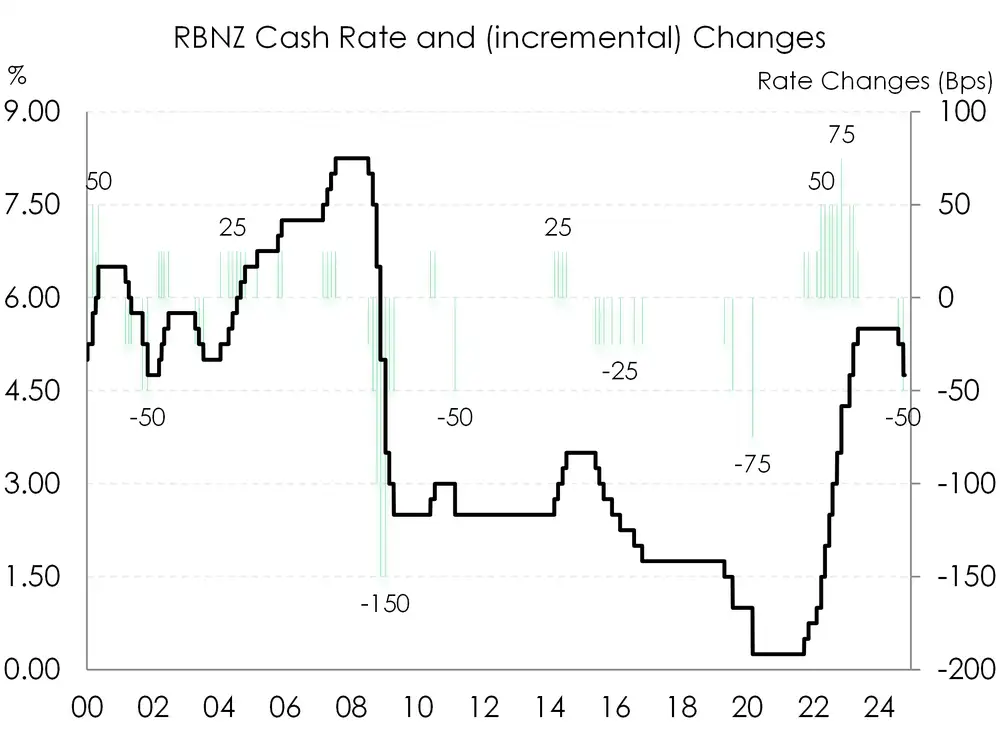

The RBNZ was very aggressive in their tightening of monetary policy, following the surge in inflation as we broke out of Covid. The RBNZ was the first major central bank to start hiking in late 2021. They started off with a few 25bp hikes, and then they delivered seven 50bps moves with one 75bp hike for good measure. The cash rate was catapulted from just 0.25%, to 5.5%. It was the hardest and fastest tightening cycle we’ve seen.

But in a recent speech, Governor Adrian Orr said “On the way down we can be more incremental, and we have been… We’re being more incremental because we’re in calmer waters but also because of that lingering inflation persistence on the domestic side.”

To us, “incremental” means a more measured pace of cuts on the way to neutral (2.75%). We think the RBNZ will deliver another 50bp move in November (to 4.25%), and they can easily justify another 50bp cut in February (to 3.75%). Cutting from 5.5% to 3.75% makes policy much less restrictive. But it will still be restrictive, and “will remain [restrictive] over the coming quarters as we get more and more confident that pricing behaviour has renormalized,” (Governor Adrian Orr). The RBNZ needs to get the cash rate below 4% ASAP. And then they can cut in 25bp increments in a search for a neutral setting.

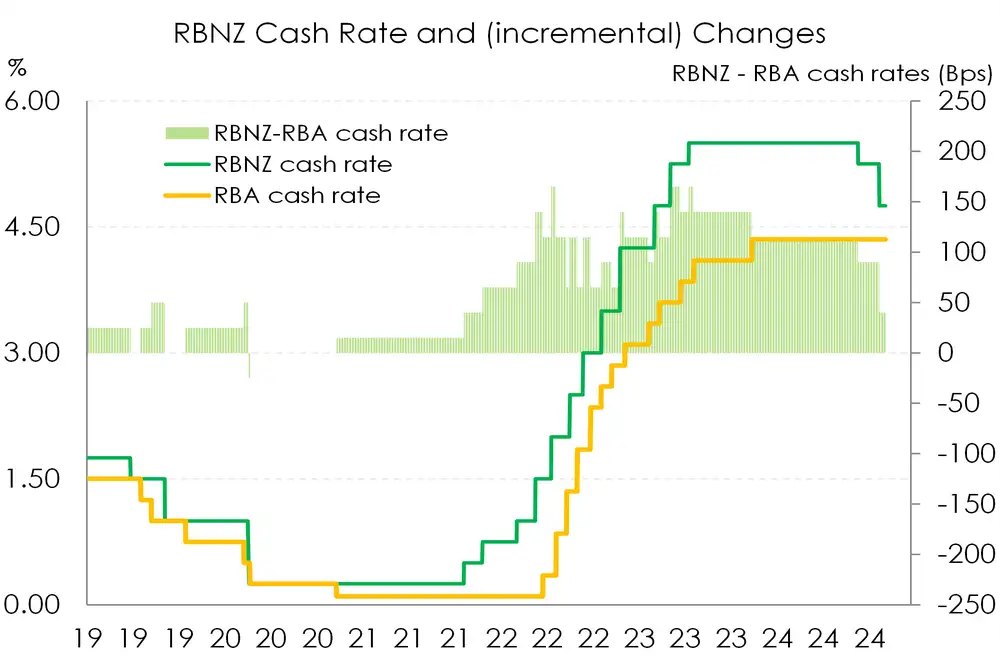

In the episode, we also discuss the growing divergence between the Aussie and Kiwi economy. And the root cause is the different monetary policy strategies taken post-Covid. The RBNZ took a hard and fast approach. It’s resulted in a sharper slowdown in economic activity, climbing unemployment, but a faster fall in inflation. The RBA, in stark contrast, went slow and steady to preserve employment gains. Less aggressive tightening has led to a more resilient economy and labour market in Australia, but a slower easing in inflation.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.