We’re forecasting a strong 5-7% increase this calendar year. Record migration flows are boosting demand for rentals, which will boost developer confidence. And house prices will be impacted by strong marginal buyer interest.

The correction we had to have, actually, the correction the RBNZ made sure we had, is ending. Surging migration, again and again, record low mortgage rates, and then the reversal, have seen property prices fluctuate wildly.

The last few months are hard to gauge at the best of times. The summer break is more for holidays than life changing decisions. But activity is showing signs of improving. And prices will follow. The new coalition Government’s policy changes are a positive.

Interest rates will play a big role. Rates may rise a little more. And then they may fall, later in the year.

House prices out of the red and into the black

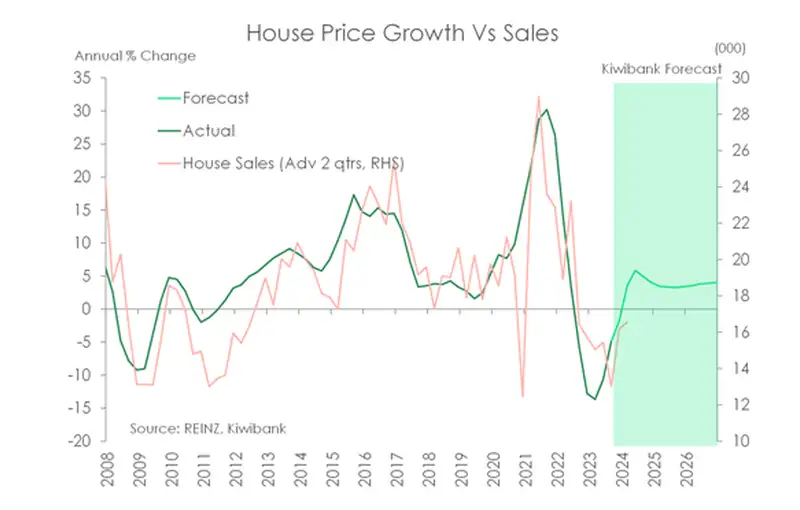

We have had a cracking summer, compared to last year. And activity in the housing market always cools over the hotter months. Fair enough. Activity dries up and active listings often come back in the new year. But according to the official REINZ data, house prices are out of the red and into the black. It has been a long time coming.

The latest data from REINZ for January, shows a positive gain in house prices of 0.4% over the month, and 2% over the year. House prices are still down over 14% from the November 2021 high. And house prices recorded a peak-to-trough correction of 17% in May last year. But the momentum has turned. And it needs to, in order to encourage investors back to invest, and developers to develop.

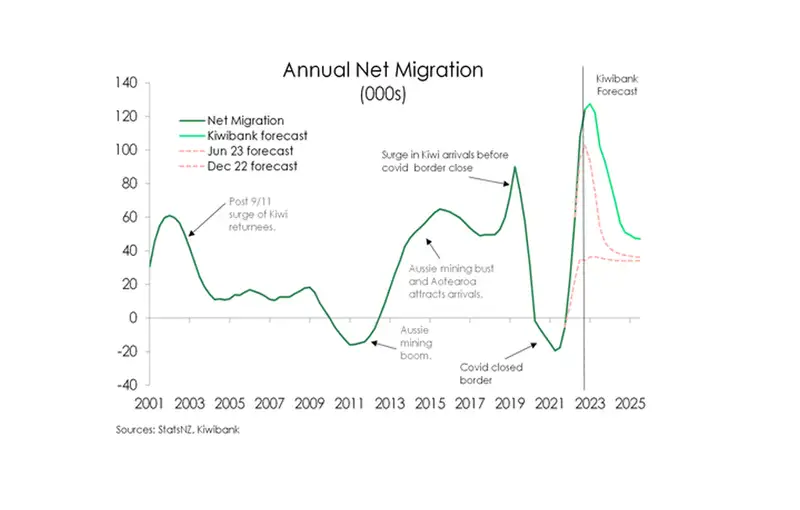

Any discussion around the Kiwi housing market must involve the migration boom. Back in 2022 we made what we thought was an assertive, well above consensus, forecast of a net 40,000 permanent migrants in 2023. We soon saw the avalanche coming, and bumped out forecast to 100,000. Again, it was well above consensus. And we ended up with 130,000… a new record intake. More people means more housing. And housing is already in short supply.

For more detail on the drivers of the Kiwi housing market, see: “Kiwi housing: all you need to know for the great BBQ debate this summer.” We talk through the monumental movements in migration, and the chronic shortage of dwellings. And we talk through our recent experiences, and the likely path forward. Basically, we have a housing shortage, exacerbated by surging migration, complicated by climate change related risks, and our policymakers focus more on demand than supply. Supply is the issue. It is increased (or elastic) supply that will better balance our housing market. It’s not about limiting demand.

So, what is happening with supply?

At a time when we need the supply of homes to surge, to meet migration demand, we’re seeing a fall in consents. Over the last year or so, the decline in housing activity and prices have seen builders scale back. It’s expensive to build in NZ, for a variety of unacceptable reasons. And developers are no longer getting the premium price they need. Pre-sales are also soft.

The good news is we’re getting builders. Our migration stats show us that the largest group of migrants are tradies. So we’re increasing our capacity to build. What we need is a stabilising in house prices – and it’s happening now – to shore up demand and therefore boost supply.

So, what can we expect?

Forecasting is as much an art as it is a science. But the data has turned north, and we can feel the lift in confidence amongst mortgage brokers, real estate agents, investors and customers. We think we’re much more likely to see price gains continue over 2024.

- The surge in migration will play a big role

- The demand/supply imbalance will worsen.

- The surge in migration and the loss of dwellings at high risk of climate change will only exacerbate the housing shortage.

- The new Government will play a big role

- Because the ‘promised’ reintroduction of interest deductibility, shortening the Brightline test timeline, and possible watering down of the CCCFA, will entice investors.

- Any added infrastructure spend or incentives for new builds will also be welcomed.

- Interest rates will also play a large role, eventually.

- We think rates will fall in 2024. But buyer beware: The RBNZ is threatening to hike again. So there may be a lift near-term.

- Our best guess is house prices will rise by 5-to-7% this year. Call it 6% to sound precise.

The forward indicators are turning positive

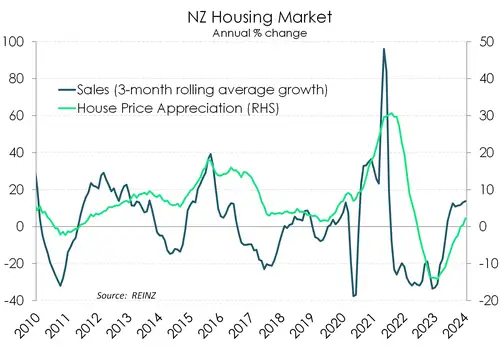

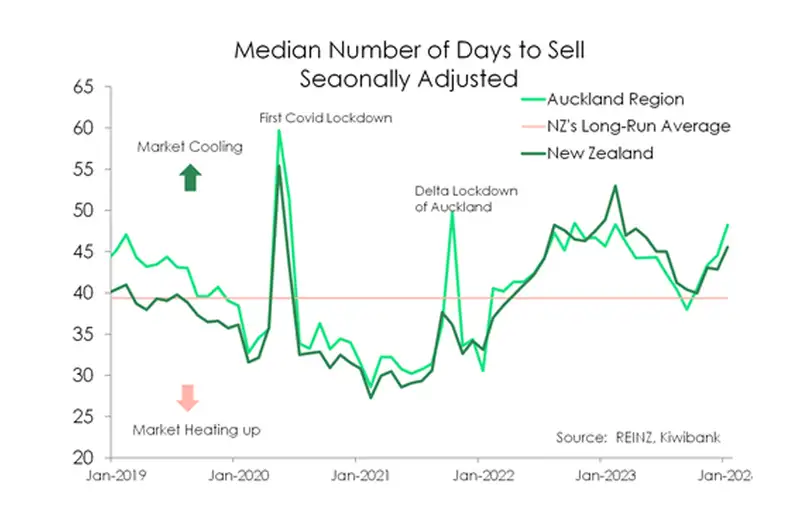

When we look at housing, there are a few high frequency indicators we like to help us gauge the strength of the market. Activity is one, days to sell is another.

“Days to sell” sounds obvious. And it is. We saw the average days to sell drop below 30 days, compared to a long-term average over 39, in the height of the 2020/21 house price boom. FOMO was very real for many would-be buyers. “You have to be quick” was heard from many real estate agents at the time. And prices kept surging.

In what was a dramatic turnaround, the days to sell blew out into 2022. The longer it takes to sell houses, the weaker the market. The “days to sell’ lengthened to over 50 days. Buyers had pulled back, and suddenly they realised they had time on their side (for a change). FOMO became FOOP (fear of overpaying). The gap between the price sellers wanted and the price buyers were willing to pay widened, with not a lot of activity in between. Prices fell.

Now, days to sell had fallen back to longer term averages. The housing market looked to be stabilising. Activity sped up. And there are more sellers meeting buyers. Sellers have reduced their expectations, and buyers are starting to pay up. Over the month of January, however, the “usual” (this is summer, chill out) seasonal lift in days to sell, was a little worse than expected. Days to sell has lifted back to 50, across Aotearoa. Seasonally adjusted days to sell, when we try to account for the usual lift, jumped to 46. In Auckland, the days to sell rose to 54, or 48 seasonally adjusted. That’s quite the move, in the wrong direction. But it is difficult to get a good understanding of the moves in quiet periods. We suspect the bounce is likely to be short-lived.

The number of transactions over the holiday period fell further than normal. Transactions are taking place, but not so much in recent weeks. In the lead up to the summer holidays, sales had bounced strongly, off low levels. It was a positive sign. Remember, house sales had fallen a whopping 37% in 2022. So we’re bouncing back. And we will get a better handle in coming months, when the market springs back into life. Where sales go, prices follow.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.