- Kiwi inflation accelerated to 2.5% over the March quarter. But the underlying trend shows consumer prices are still cooling and making good progress.

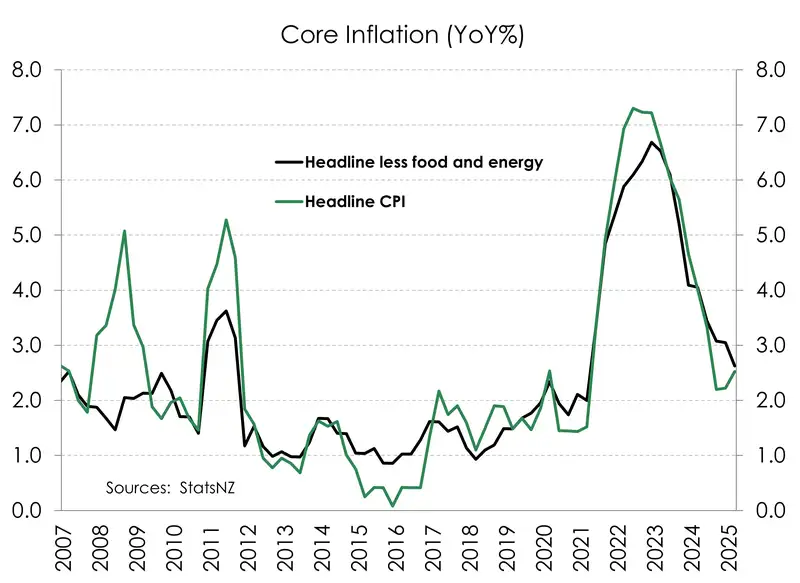

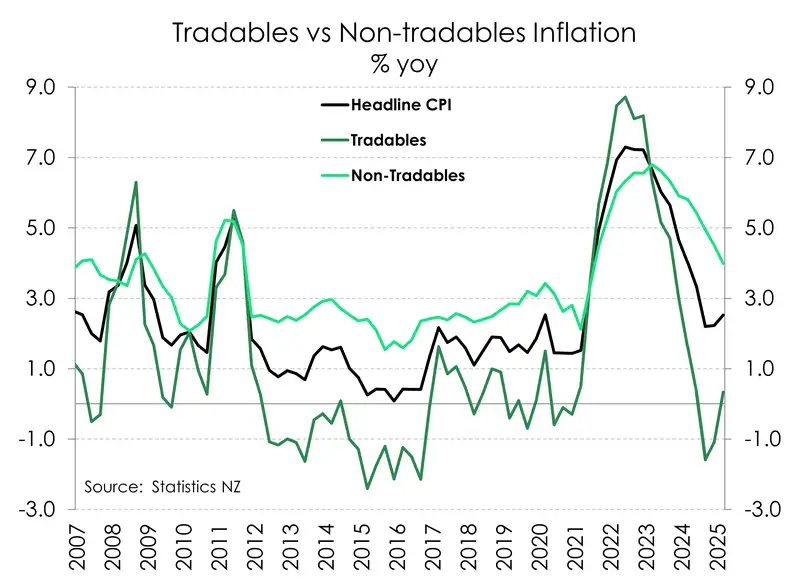

- Core inflation is back below 3%. Non-tradables inflation has eased to 4% moving further away from its 6.8% peak. And services inflation has also dipped lower. It’s all good news.

- Downside risks to medium-term inflation are growing. Whether that’s a consequence of a slowdown in global economic growth or a diversion of trade marked at a discount. The case is strong for more accommodative interest rate settings.

Kiwi inflation accelerated over the March quarter. Annual headline lifted to 2.5% from 2.2%. While it’s a move in the wrong direction, there’s no need to panic at the monetary policy HQ. Inflation remains within the RBNZ’s 1-3% target band. And, most importantly, the underlying trend in consumer prices continues to be one of cooling. Excluding the volatile movements in food and fuel, annual core inflation has fallen to 2.6% - the first time below 3% since March 2021.

Today’s report showed that price increases are becoming less extreme. More than half (55%) of all goods and services increased in price, similar to last year. However, the March quarter saw the lowest proportion (23%) of the CPI basket increase by more than 5% in the last four years. June 2023 marked the high, as 59% of the basket faced more than a 5% price increase.

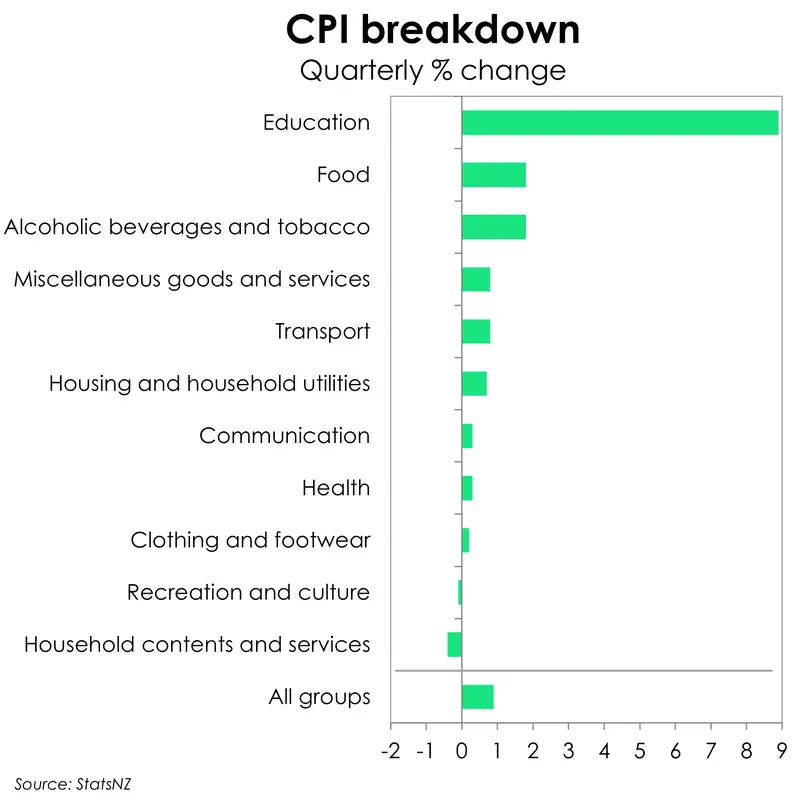

Consumer prices rose 0.9% over the March quarter. The 4.6% increase in petrol prices was the largest contributor. A seasonal rise in food prices was another key driver, specifically, the 5.6% increase in milk, cheese and eggs. Falls in prices for international airfares as well as some discounting across games and toys provided some offset.

Domestically generated inflation was stronger than expected, up 1.1% over the quarter, largely due to the introduction of the Final-year Fees Free scheme (which replaced the first-year fees free scheme). Essentially the change has resulted in more students paying the full cost of study, which explains the 22.6% whopper of a price increase. Educaytion is clearly a good only domestically consumed, so it is inflating the non-tradables numbers slightly. But we take comfort in the other components of domestic inflation which continue to cool. Annual non-tradables has fallen to 4% from 4.5%, and peeling further away from the 6.8% peak.

Rental inflation, which is one of the largest weighted items (11%) in the CPI basket, rose just 0.7% over the quarter – the lowest for a March quarter since 2021. And for the first time since 2021, annual rent increased by less than 4% (at 3.7%). Home construction costs also continue to cool significantly, dropping to 1.9% - the lowest since September 2010. There are still some lingering frustrations, especially when it comes to council rates and insurance. Nonetheless, domestic price pressures, in aggregate, are cooling.

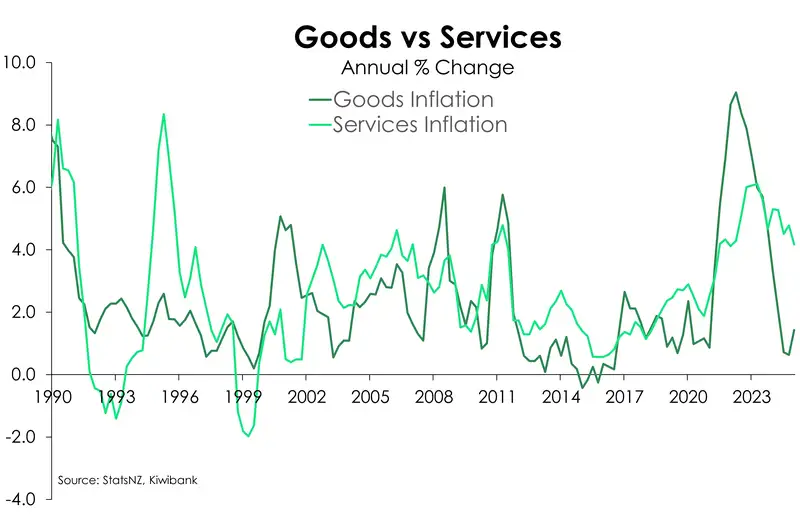

Also reflective of a weakening economy and labour market is the continued slowing in services inflation. Wage growth has eased significantly. As a result, services inflation has fallen from 4.8% to 4.2%. A further softening of the labour market is expected, which will keep downward pressure on services inflation. Goods inflation, however, broke 10 straight quarters of disinflation, with a lift from 0.6%yoy to 1.4%yoy.

The lift in imported inflation was as expected, up 0.8% over the quarter. The annual rate continues to creep higher, from -1.1% to 0.3%. Higher dairy and meat prices over the year underpins the increase, offset slightly by a fall in petrol and vege prices.

Looking at the CPI report card, there's enough disinflation in the data to support further rate cuts from the RBNZ. The prospect of a global trade war will also likely keep downward pressure on prices. Whether that’s a consequence of a slowdown in global economic growth or a diversion of trade marked at a discount. Downside risks to medium-term inflation are growing. And so the case for more accommodative interest rate settings is strengthening. More is needed from the RBNZ to stimulate the recovery into 2026 and beyond. We believe households and businesses need rate relief. We expect the RBNZ to deliver another 100bps of rate cuts to a 2.5% cash rate by the end of the year.

Basket breakdown

Once again, persistent price pressures over the past year were concentrated around rental and council rate inflation. While rental inflation has continued to cool from its peak of 4.8% in June 2024, it still rose by 3.7% in the 12 months to March. And given its significant weight in the CPI basket, this increase was still the largest contributor to annual inflation, accounting for 14.3% of the total yearly rise.

Similarly, council rates—up 12.2% over the year—also contributed 14% to the overall 2.5% increase in prices. While on the other hand, lower petrol prices were the biggest offsetting factor, falling 2.8% over the year and no doubt helped by the removal of the Auckland regional fuel tax.

Over the quarter however, rising petrol prices, up 4.6%, was the biggest contributor to the 0.9% quarterly lift in prices. A lower Kiwi dollar over the quarter would have been partially responsible for the move. Meanwhile, Tertiary education costs, with the changes around fees free, also surged. And the 22.6% increase across tertiary education contributed 11% to the quarterly lift. Providing some relief, international airfares down 7.7% over Q1 subtracted 15% from the quarterly move. While games, toys, and hobbies, down 7.1%, removed another 5.5%.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.