The Kiwi dollar

The purchasing power of all Kiwis rises with a strengthening Kiwi dollar. If you want to travel abroad, or simply buy a foreign made good, a rising Kiwi helps. On the flip side, Kiwi exporters want a weaker Kiwi dollar to make their goods and services cheaper to foreign buyers. Fonterra farmers benefit from a falling Kiwi, so do tourism operators. So we all have an interest in the Kiwi. But forecasting where the flightless bird will land in the next 6-12 months is as difficult as it gets.

The Kiwi is the most volatile developed market currency. Basically, it bounces around wildly. And at times, it has little regard for economic fundamentals. But in order to forecast, the economic fundamentals can help. There are two major drivers of our currency: the terms of trade, and interest rate differentials. Other factors like current account deficits and sovereign risk come into play over a longer time frame. Will we default? No, so we move on.

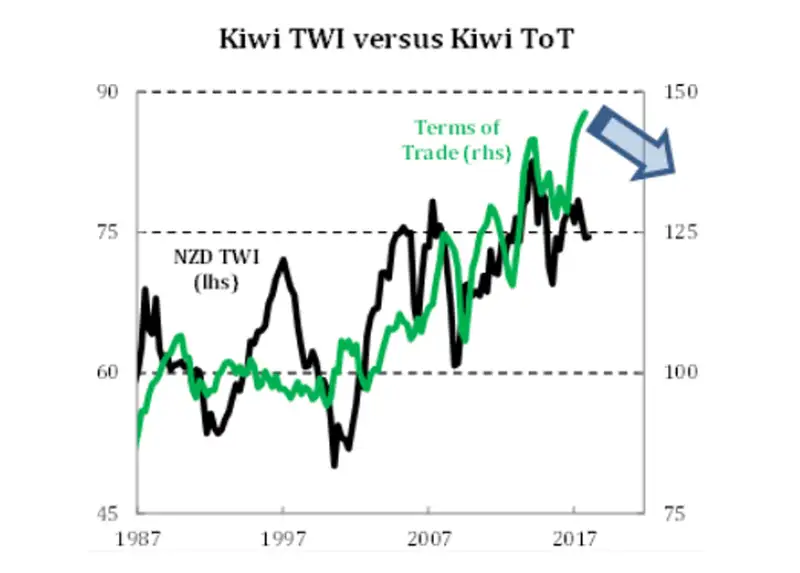

The first driver of the flying Kiwi, is relative trade prices

Our terms of trade, is economist speak for prices we receive for our exports, versus prices we pay for our imports. A currency is simply a relative price. Our currency versus their currency. So, the relative prices of imports versus exports is important. When dairy prices rise relative to petrol prices, we are better off (as a whole). Right now, dairy prices are rising relative of petrol prices, underpinning some of the Kiwi dollar’s strength. Our best guess is imported prices start to rise, ever so gradually, as global growth improves. We also expect our export prices to moderate slightly, as supply improves. So we expect our terms of trade to ease a little. A lower terms of trade should lower the Kiwi. Good news for exporters.

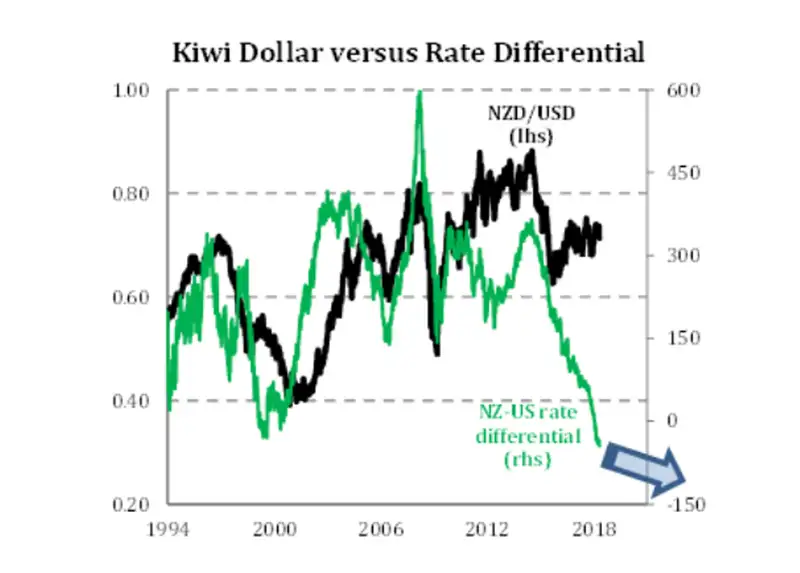

The second major driver of the Kiwi is interest rate differentials

Are our interest rates higher or lower than other nations? And where are they headed? Well, for the first time in almost 20 years, Kiwi interest rates are below US interest rates. Previously, our currency has fallen sharply during periods of falling and negative rate differentials. Foreign buyers of Kiwi dollars do so for a variety of reasons, but the most compelling is “extra income”. They want to earn a higher interest rate here relative to other parts of the world. Historically, New Zealand provides a much higher rate of return. We’re relatively young, and tend to grow faster than more developed nations – until recently. The so called “carry trade” is a much loved Japanese strategy. Take money from Japan, where they get nothing for it (or even negative interest rates) and plant it in Australia and New Zealand where they get much more than most. As the “extra” income they receive in New Zealand evaporates, compared to the US, they tend to invest less in New Zealand – lowering the demand for our dollar. The global interest rate outlook points to a modest fall in the Kiwi this year.

So where to from here?

The easing in our terms of trade alongside a deepening decline in our interest rate differentials, should mean a weaker Kiwi dollar. But the Kiwi dollar has two parts: Kiwi on one side, and (USD) dollar on the other. The USD is the bigger part. And with Trump at the helm, calling a stronger USD (weaker NZD) it’s fraught with fire and fury, and danger.

Of course the other fun currency cross to follow is the Kiwi/Aussie. Punting on the Kiwi/Aussie cross can be fraught with danger. Many a trader has been buried by the volatility. The NZD/AUD seduces you into thinking it trades beautifully, and even makes sense. And it does, until it doesn’t. The relative size of Australia versus New Zealand means our currency is much less liquid (doesn’t have as much flow going through it). So given we are talking about a relative price, the Aussie price can hold better than ours, and ours is more volatile. So NZD/AUD can do anything in stressed markets. You can’t rely on it. Our best guess for the NZD/AUD, is a slight depreciation in the Kiwi relative to the Aussie. Unless of course the fair play Aussies use a bit of gold sandpaper to rough up their currency against ours. Underarm tactics aside, we expect both ANZAC economies to see a slight fall in their currencies against the USD. We see the NZD falling to 70c against the USD by year end. And we expect a further depreciation to 67c in 2019. Not a large move, but it’s a move in the right direction. We see the NZD/AUD easing towards 90c, and possibly 87c over the same period.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.