“Give me a word. Give me a sign. Show me where to look. Tell me, what will I find?” Collective Soul

- 2022 will (hopefully) come with greater freedoms, and international travel. The Kiwi economy is well placed, well oiled, and well prepared for another year of solid growth.

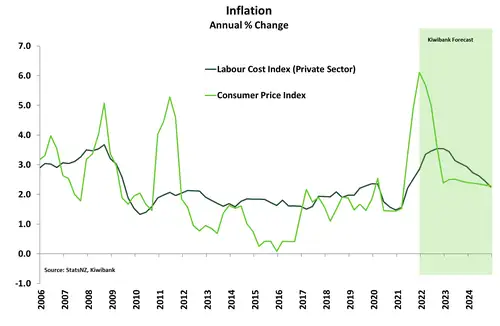

- Inflation is the big risk for 2022, with surging costs domestically and rising wages.

- Businesses will have to contend with rising costs, rising interest rates and a rising Kiwi dollar.

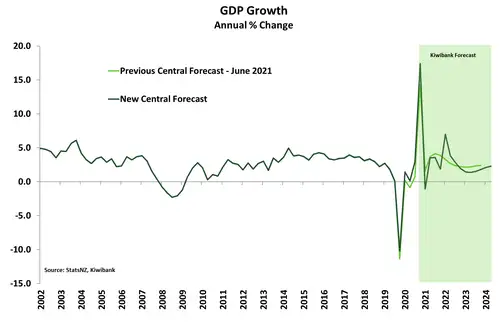

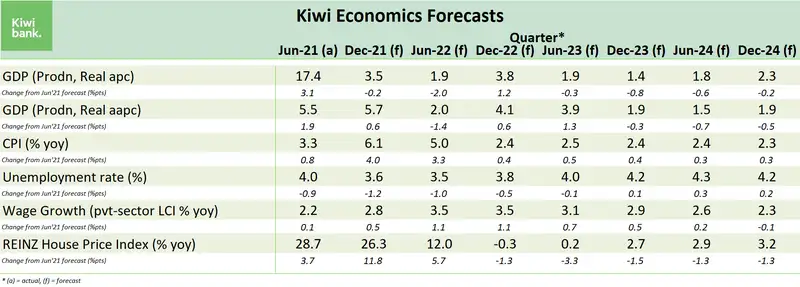

The Kiwi economy has been well-supported by rising house prices, resilient household consumption and robust demand for our exports. Economic activity has returned to pre-Covid levels. The latest lockdown will be a step-back, but only temporarily. Activity has picked up strongly, doing well to make up for weeks of thumb-twiddling. And demand has simply been deferred. Consumer spending rebounded once restrictions were relaxed. 2022 is also expected to be the year of international travel. The long-awaited revival of the tourism and education sectors should see a bigger contribution from these sectors next year. We expect the Kiwi economy to grow at a solid 4.1% over 2022.

However, there’s cause to be cautious. Covid and its yet-to-be-discovered mutations will continue to plague confidence. The emergence and outbreak of Omicron is a timely reminder that the pandemic is not yet over. However, Covid-related restrictions are proving to have a diminishing economic impact. Businesses and households have adapted and are better prepared. It would take a considerably worse disruption than what we’ve experienced to materially derail the economy.

Here’s our key economic considerations for 2022:

- Economic activity: will rebound strongly following the Delta disruption as underlying demand remains robust. But Covid is still the biggest headwind for the Kiwi economy. Rising interest rates and weaker real incomes also challenge the resilience of household consumption and business investment.

- Inflation: will rise further as cost pressures remain acute. Supply-driven inflation will eventually abate, as global supply chains are unclogged, but there’s growing concern over domestically generated inflation. Wages are on the rise with super-tight labour markets and high inflation.

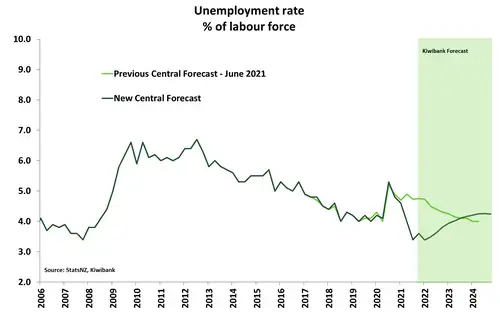

- Labour market: will remain tight by historical standards, with the unemployment rate starting 2022 at a record equalling 3.4%. Hiring intentions have intensified and job vacancies are well above pre-Covid levels. The reopening of the border might be a double-edged sword, with Kiwis leaving as migrants enter.

- Housing: is set for a period of consolidation. Rising mortgage rates, tighter LVRs, tax changes, tougher access to credit, and (most importantly) more housing supply coming to market – will weigh on prices. There’s material chance of a modest market correction – house price falls.

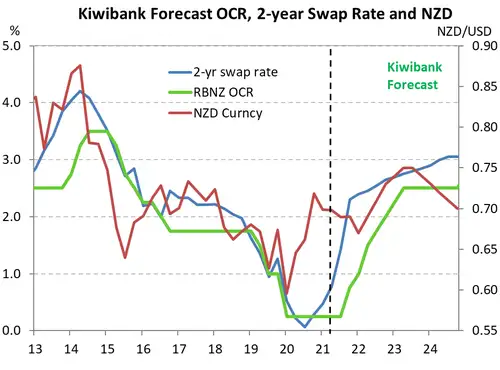

Given the state of the Kiwi economy, emergency settings of low interest rates are no longer needed. The RBNZ will continue to normalise monetary policy settings over 2022.

Here’s our thoughts on interest rates and the Kiwi over 2022:

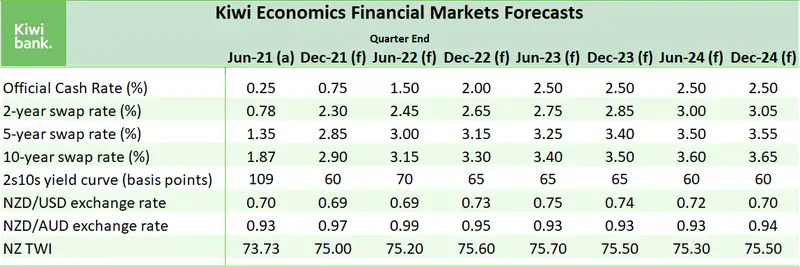

- Interest rates: will continue to rise. The current cash rate of 0.75% has at least another 175bps of hikes in the pipeline. The RBNZ has signalled a tightening path to at least 2.5%. All lending and savings rates will continue to push higher.

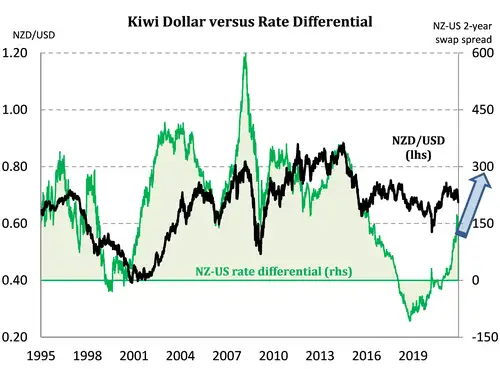

- Kiwi exchange rate: is undervalued. We expect to see a stronger Kiwi, with record high terms of trade and supportive interest rate differentials. Upside to the exchange rate however is capped, should other central banks follow in the RBNZ’s footsteps.

An economy stuck in overdrive

The Kiwi economy has been well-supported by rising house prices, resilient household consumption and robust demand for our exports. The latest lockdown will be a step-back, but only temporarily. We expect the economy to contract by around 4.5% in Q3 – far smaller than the 11% decline last year. Auckland, however, was still locked down in October, taking some of the shine off the Q4 rebound. We’re expecting a 3.6% quarterly jump in Q4.

The rebound will continue in 2022. 2022 is expected to be the year of international travel. The long-awaited revival of the tourism and education sectors should provide a decent boost to activity next year. Tourists still want to cross NZ off their bucket list, and our universities are still world-ranking. We expect the Kiwi economy to grow 4.1% over 2022.

The Kiwi economy is running above its potential. And a positive output gap (the difference between what the economy can produce and what it does produce) means further upside to employment, inflation and wage growth.

The Kiwi labour market has never been tighter. The unemployment rate has plunged to a record low of 3.4%, despite participation rising to a record high of 71.2%. Basically, if you want a job (within reason), there’s one for you. Leading indicators suggest that the labour market is set to tighten further. Hiring intentions have intensified, job vacancies are well above pre-Covid levels, and expected labour turnover has hit a 50-year high – all this despite the Delta outbreak. However, we do expect to see some, but limited, fallout on the labour market from the latest lockdown. We forecast the unemployment rate to lift modestly to 3.6% in the Dec-21 quarter, with restrictions having dragged on in Auckland – 30% of our workforce. Beyond Q4, the unemployment rate is expected to fall back to the record equally low of 3.4%. The current skills mismatch however means the unemployment rate might struggle to sustain a rate in the low 3s.

Given the closed border, the pool of available workers is limited to homegrown talent. And with employment already above its maximum sustainable level, that pool is quickly drying up. Acute labour and skill shortages means employers are having to pay up to attract and retain workers. High labour turnover suggests employees are leveraging their improved bargaining power to switch jobs for bigger paychecks. Wage growth is already up 2.5% compared to Q3 last year – the fastest rate in over a decade. Also underpinning rising wage growth is the expectation inflation will remain elevated. Inflation has spiked to a 10-year high. Consumer prices are up almost 5% over last year, and the price gains have been broad-based.

Annual inflation is expected to peak in Q4 at just over 6%, and remain above the RB’s target band for most of 2022. The costs pressures brought on by disrupted global supply chains will see repeated large price gains in the Dec-21 and Mar-21 quarters. The recent surge in energy and other commodity prices is also yet to feed into the consumer level. However, the rampant rise in shipping costs looks to have ended, and shipping costs are actually falling now. We should see broad-based inflation pull back over 2022.

Rising inflation means the cost of living has and will become even more expensive. And workers will demand compensation. With inflation at 5%, it’ll take a bigger pay rise for households to feel better off. Wage inflation is forecast to continue rising and peak at over 3.5% in the middle of next year before easing in line with general inflation. From a price stability perspective, alarm bells at the Reserve Bank will start to ring if higher inflation becomes embedded in wage-price setting behaviour. Medium-term (5-year ahead) inflation expectations will be closely watched and have already risen to 2.17% from 2.03%.

The housing market has a substantial influence on the economy. Housing is our largest asset class. And the effect of rising housing wealth stimulates consumption. When house prices are rising, households feel more inclined to spend. Moreover, households are more inclined to invest in their largest source of wealth. In a high-demand environment, developers also see an opportunity to profit, boosting construction activity too. Since the start of the pandemic, housing wealth, at least on paper, has risen by many hundreds of billions of dollars.

Cautious consolidation

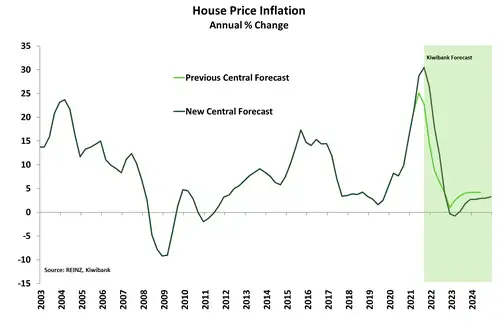

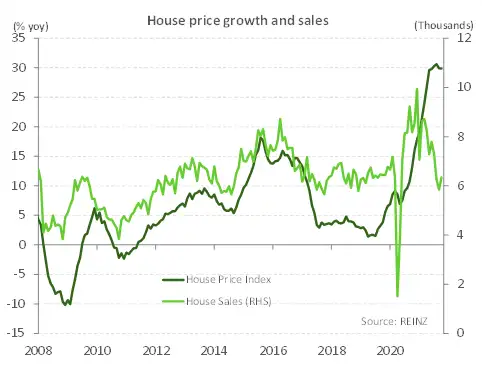

After a year of unsustainable price growth, the housing market is set for a period of consolidation. And consolidation means a strong likelihood of house price falls – albeit modest. The housing market has been propelled by a heady mix of rocket fuelled cheap borrowing costs, a significant housing shortage, and solid employment growth. According to the REINZ house price index (HPI), house price growth peaked at an all-time high of 30.5% in the September quarter. However, this rocket fuel is now running dry. From here, we expect to see house price growth falling fast as an increasing list of headwinds pound the market.

Mortgage rates have risen rapidly since the middle of the year. And mortgage rates have further to rise (see the financial markets section below). Finding a carded 2-year fixed mortgage rate below 4% is now nigh on impossible. At the start of the year, with the prospect of a negative cash rate, a 2-year rate in the low 2s was common. Increasing mortgage rates have driven up the cost of servicing a mortgage. Disposable incomes will be reduced as mortgage holders roll off record low mortgage rates. More importantly, rising mortgage rates reduce the amount that households can borrow, lowering their potential bids. For sellers, a quick sale may mean lowering their price expectation. Rising mortgage rates are a clear coolant on housing demand.

Another coolant on demand has been numerous housing-specific policy changes introduced this year. The Government announced back in March, tax changes targeting investors. The changes included tightening the bright-line test and removing the tax deductibility of interest expenses. The RBNZ got in behind the call to restrain investor exuberance by tightening investor loan-to-value ratio (LVR) restrictions. The share of lending going to investors fell soon after. Since then, LVRs have been tightened for owner-occupiers too. Finally, and perhaps somewhat unintentionally, recent changes to the Credit Contracts and Consumer Finance Act (CCCFA) will likely reduce credit availability. The legislative changes that came into effect from 1 December put increased onus on banks to demonstrate borrowers can afford a mortgage. Failure to comply comes with the threat of large fines. Lenders will probably err on the side of caution when it comes to riskier borrowers and deny credit.

Supply is also set to weigh on house prices over the year ahead. A record 47,715 new dwellings were consented in the 12 months to October – that’s up 26% on the year. The lift in housing supply has occurred at a time when a closed border has seen population growth plummet. Looking ahead, a cooling housing market combined with the capacity and labour constraints in the building industry will likely cap the rate of home building somewhat. We don’t see an immediate flood of properties if the new housing densification strategy is approved.

A reasonable predictor of house price growth is sales activity. But since late last year, sales have fallen while house prices have sustained record highs. The reason why has to do with record low levels of listed property. A combination of the housing shortage, and the psychology of a bull property market. Selling in a market with limited supply risks not being able to buy back in. Sellers risk watching possible juicy capital gains slip away and, when re-entering the market, having to accept a lower rung on the property ladder. A similar psychology also drives eager first home buyers – so called “Fear of Missing Out” (FOMO).

However, the dynamics in the market are starting to change. The number of new property listings are trending higher compared to recent years. And a lift in new listings is particularly noticeable in regions in the lower North Island such as Wellington, Whanganui/Manawatū, and the Hawke’s Bay – previous bastions of market enthusiasm. As the market fails to absorb the new listings, properties hang around for longer and the market becomes a buyers’ one. We are forecasting very modest house price falls this time next year. Somewhere in the order of -0.5-to -1%. More of a consolidation rather than a correction. Other forecasters, such as the RBNZ, see much larger falls ahead. However, looking at the past 30 years meaningful corrections typically occur when credit conditions tighten rapidly, and we have an unemployment rate rising fast. Looking ahead we certainly have tightening credit conditions and rising mortgage rates. Yet over our forecast period the labour market is a source of strength in the economy not weakness. The unemployment rate is expected to remain consistent with what would be considered consistent with full employment. We are reluctant to project sustained house price falls as a result.

A grand reopening of sorts

After almost two years of Covid-related restrictions, the NZ border is finally set to reopen. The doors aren’t being flung open though, just creaked open to start with. But it is a start. From mid-January, MIQ requirements will begin to be removed, starting with travel to and from Australia. Instead of an extended stay in MIQ on arrival, eligible vaccinated travellers will only need to self-isolate for seven days. And if arrivals pass the standard Covid tests they will be able to enter the community, assuming the Omicron strain of Covid doesn’t mess things up. The announcement provides a light at the end of a long tunnel for tourism.

Opening the border has two key influences on the economy. The first is on net migration, which is a key driver of NZ’s population growth, medium-term demand, and labour supply. And second, services exports such as tourism and education. The initial impact on net migration is uncertain. We may see an initial jump in long-term departures, as those itching to go on an OE will be comforted knowing they won’t be shut out of Aotearoa by a lottery of MIQ spots. However, over 2022 we expect to see net migration begin to lift as NZ’s overly tight labour market attracts people in to plug skills gaps. Our view throughout Covid has been that when net migration does recover, it’s unlikely to get back to the highs seen pre-Covid of an average of around 60,000 per annum. The Government has already signalled a tightening of immigration policy and we are picking a peak in net migration of around 30,000 over the medium term. A lower peak in net migration means the construction sector is better placed to meet the demand for housing.

For the tourism industry, the planned changes are unlikely to provide as much of a boost for tourism operators as might be hoped for. From 30 April anyone fully vaxxed can plan a trip to Aotearoa. However, NZ is a long (and expensive) way to travel to spend the first seven days stuck in a hotel. Self-isolation requirements will likely put off many. We should see more trans-Tasman tourists here visiting relations. Unfortunately, these visitors don’t tend to spend as much on seeing the sights. The focus tends to be more on spending time with friends and family. The education sector will likely fare better, as a seven-day isolation period is less of a disruption for someone studying toward a multi-year qualification.

The end of cheap money

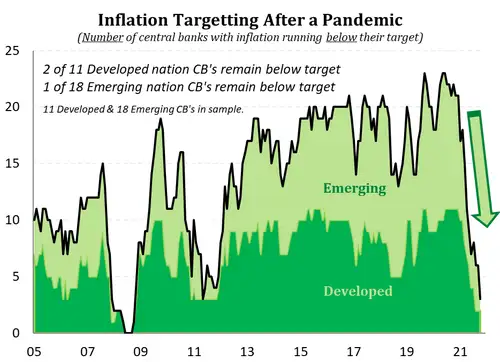

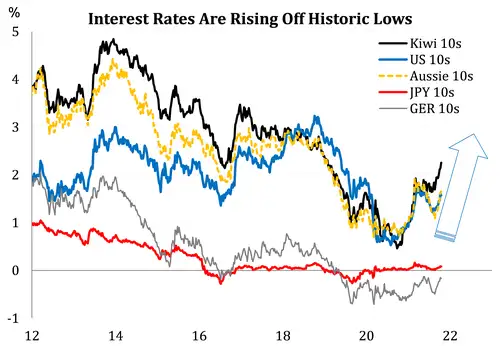

Interest rates have risen around the world, but remain at very low levels. Given the spike in global inflation, interest rates are destined to rise swiftly next year. Over the last 15 years, inflation has consistently surprised on the low side. Ageing populations, forever cheaper technology, and ecommerce giants (like Amazon) have put downward pressure on prices. It was only prior to the 2008 GFC where we saw inflation running above central bank mandates. Yeah, that was short lived…

Just last year, all developed world central banks and most emerging world central banks had inflation running below target. 2020 was looking awful. One year on, and inflation has exploded. Of the 11 developed world central banks in our sample, 2 have inflation running below target (Switzerland and Japan). 9 have inflation running above their mandated targets (generally 2%). Most have yet to commence policy tightening, including the US Fed (inflation at 6%), the RBA, the ECB and BoE. And it is not just a developed world problem. Of the 18 emerging world central banks, only 1 has inflation running below target (Indonesia).

Most of the global inflation pressure can be put down to strong demand, disrupted supply and high commodity prices. The disrupted supply looks transitory. But the domestically generated inflation is on the rise also – with tightening labour markets and rising wages. Almost all central banks remain cautious. Almost all central banks are well behind the RBNZ. And almost all central banks will find themselves lifting interest rates next year.

As central banks around the world start lifting their cash rates, to combat inflation and return policy to more normal settings, all interest rates will push higher. And global interest rate moves will put further upward pressure on Kiwi interest rates (beyond 5 years). The likely (upward) move in global interest rates comes at a time when the RBNZ is already in hot pursuit.

The record low interest rates of earlier in the year, even lower than the lows of the 1950s, are no more. The time of cheap money is over. The RBNZ is normalising policy, by taking interest rates back to more normal levels. Wholesale rates markets have factored in the higher rate path. And the wholesale funding costs for banks have risen sharply. Mortgage rates have risen in response, and we expect to see further hikes from here. The current cash rate of 0.75% has at least another 175bps of hikes in the pipeline. A cash rate of ~2% is considered neutral (neither tight, nor loose). The RBNZ’s OCR track implies, for the first time in a very long time, that the RBNZ will need to tighten policy through neutral to contain the economy, esp. housing. The RBNZ has signalled a tightening path to at least 2.5%.

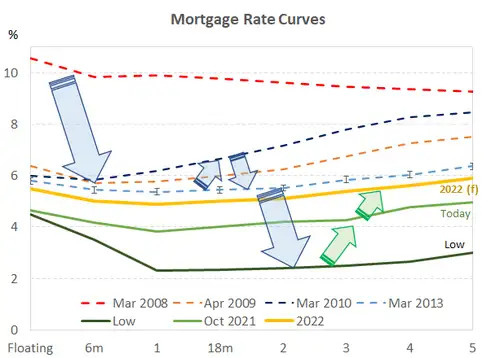

The Kiwi mortgage curve has moved a lot since 2008. Prior to the GFC of 2008, mortgage rates peaked above 10%. The carnage of the financial crisis saw mortgage rates slashed towards 6%. Mortgage rates then fluctuated for years but hit an air pocket with Covid. The Covid pandemic saw mortgage rates slashed further, down to the lowest levels in history. The emergency settings were designed to insulate an economy in lockdown. The economy proved to be far more resilient, however, and house prices rose an unsustainable 30% over the last year. There's no longer a need for emergency settings.

Now, mortgage rates are rising back to 'more normal' levels. The green line in the chart below shows the average mortgage rates currently on offer. And the yellow line shows our forecast for mortgage rates over the next year. Most fixed mortgage rates will be 2-2.5%pts higher than the record lows recorded earlier this year. These higher mortgage rates come at an awkward time.

70% of outstanding mortgages are due to roll over in the next year. 70% of mortgagees will potentially face much higher mortgage rates as their loan rolls over. Because mortgage rates have since lifted considerably, and are likely to continue rising from here.

The impact on discretionary spending will need monitoring, with higher debt levels and higher interest rates. Households have taken on more debt and will be more sensitive to rate rises.

Kiwi currency still looks strong

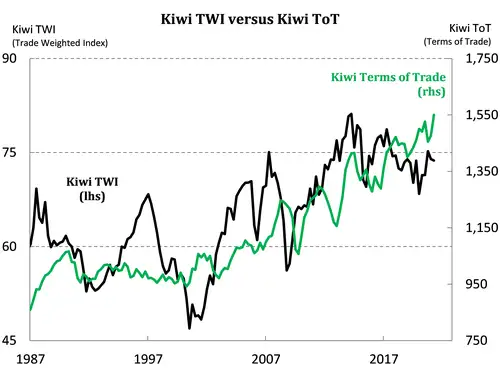

There are two key drivers of our Kiwi dollar forecast, the terms of trade (export prices relative to import prices) and interest rate differentials. NZ’s terms of trade is at record highs, suggesting our currency is undervalued. We do, however, expect the terms of trade to wane a little over 2022. The softer trajectory suggests a lower peak in the NZD. We have lowered our forecast for the NZD accordingly.

When it comes to interest rate differentials, the RBNZ is well ahead. We continue to see our interest rates rising at a faster clip than those offshore. The wider differential continues to point to a stronger Kiwi dollar.

Our forecast for the Kiwi looks for some near-term weakness, as the RBNZ does not come back into play until February, and the Omicron variant poses risks. But over the year ahead, we forecast the Kiwi to regain some strength. We forecast the Kiwi dollar to hit 0.73c next year and peak possibly as high as 75c into 2023. The Kiwi flyer’s ascent however is capped, should the Fed tighten policy more aggressively. In November, Fed Chair Powell said that rate hikes in 2022 were “extremely unlikely”. However, US inflation is running at 6%, with further upside. And Powell has since relocated from camp “transitory” to camp “persistent”. Rate hikes in 2022 are no longer “extremely unlikely”. There’s downside risk to the Kiwi exchange rate with central banks (inevitably) following the RBNZ’s footsteps.

We note that predicting the volatile Kiwi currency is fraught with danger. We expect to see a wide range in the Kiwi between a low of around 63c and a high of as much as 75c. That’s our way of saying (again), we have great unconviction in our Kiwi forecast.

All content is general commentary, research and information only and isn’t financial or investment advice. This information doesn’t take into account your objectives, financial situation or needs, and its contents shouldn’t be relied on or used as a basis for entering into any products described in it. The views expressed are those of the authors and are based on information reasonably believed but not warranted to be or remain correct. Any views or information, while given in good faith, aren’t necessarily the views of Kiwibank Limited and are given with an express disclaimer of responsibility. Except where contrary to law, Kiwibank and its related entities aren’t liable for the information and no right of action shall arise or can be taken against any of the authors, Kiwibank Limited or its employees either directly or indirectly as a result of any views expressed from this information.